Rent Debt in America: Stabilizing Renters Is Key to Equitable Recovery

Our rent debt dashboard, produced in partnership with the Right to the City Alliance, equips policymakers and advocates with data on the extent and nature of rent debt in their communities to inform policies to eliminate debt and prevent the looming crisis of mass eviction.

By Sarah Treuhaft, Michelle Huang, Alex Ramiller, Justin Scoggins, Abbie Langston, and Selena Tan

Mounting rent debt and the potential for mass eviction is one of the most pressing equity issues created by the Covid-19 pandemic. The vast majority of the millions of renters who are in debt are low-wage workers — disproportionately people of color — who’ve suffered job and income losses due to the pandemic. With the Supreme Court’s invalidation of the federal emergency eviction moratorium on August 26, 2021, these renters are at imminent risk of eviction and homelessness. Allowing an eviction tsunami to take place would be a moral travesty and a policy failure that would deepen inequities at a moment when the federal government has prioritized addressing systemic racism and ensuring an equitable recovery.

To inform policymaking and advocacy to prevent eviction and eliminate rent debt, the National Equity Atlas and the Right to the City Alliance — a network of community-based organizations working in 45 cities and 26 states to prevent displacement, expand affordable housing, and build just, sustainable cities for all — launched this rent debt dashboard in April 2021.

The dashboard provides current data on the number and characteristics of renters behind on rent for the US, states, and 15 metro areas, as well as estimates of the amount of back rent owed. With this release, we’ve added a new “Relief Map” to the dashboard tracking the distribution of federal emergency rental assistance in states, counties, and cities. We’ve also expanded our rent debt estimates to cover all states and counties in the US as well as 562 cities. To provide disaggregated data for sub-national geographies, we combine the two most recent waves of the Census Bureau’s Household Pulse Survey and use the individual-level microdata in the Pulse public-use file, which is released two weeks after the tabular data. The dashboard data is refreshed approximately every two weeks. Find our full methodology here.

This analysis shares key insights from the dashboard, incorporating data from the July 21 - August 2 Pulse survey, along with action steps that local, state, and federal policymakers must take immediately to keep people in their homes.

This is an update to our April 21, May 25, July 7, and August 10 analyses. The next dashboard update will be directly after the September 8 microdata release.

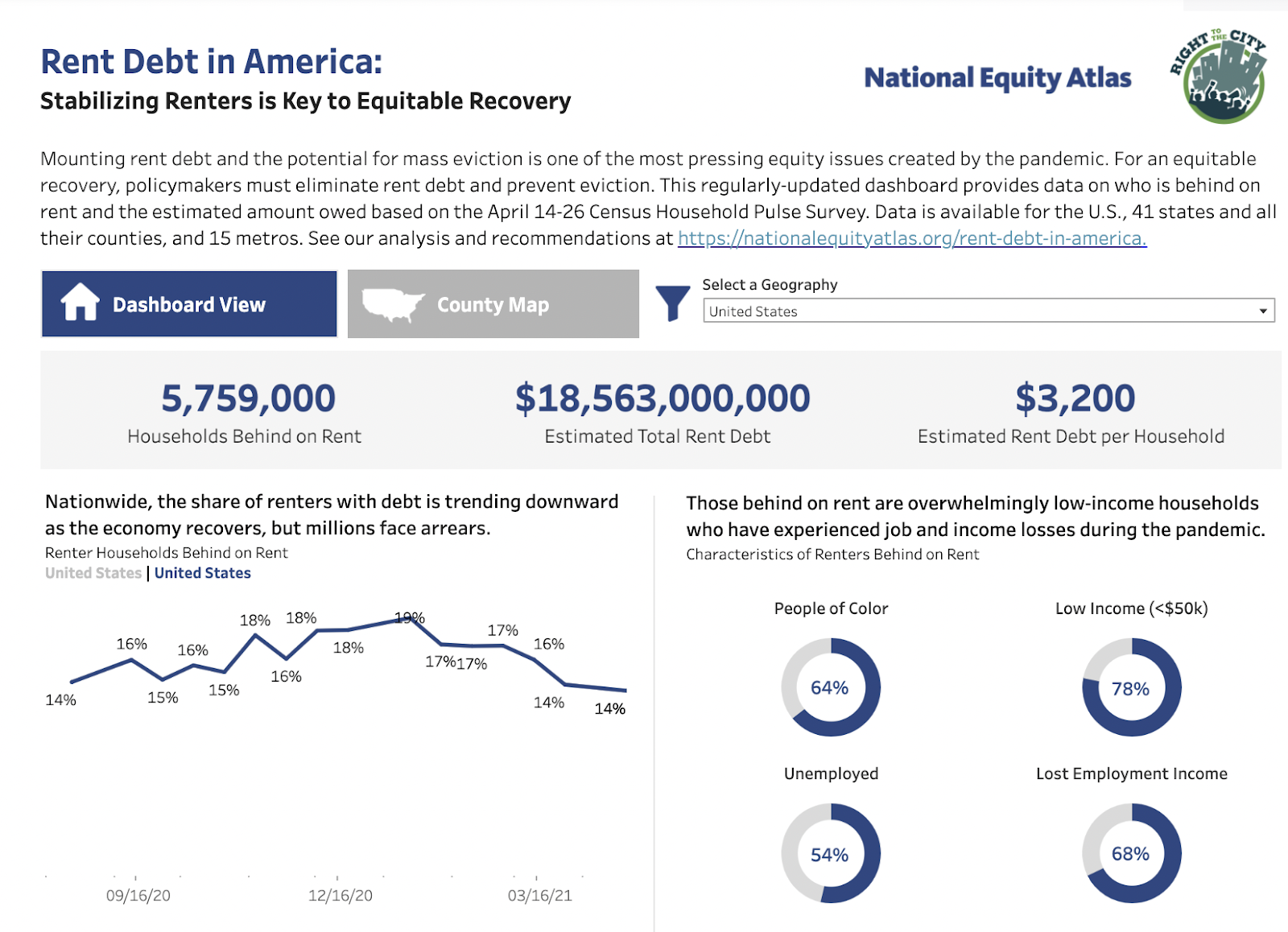

Rent debt remains at crisis levels: more than 6 million households are behind on rent, including about 7 million children.

As of the first week of August 2021, 6.2 million renter households — 15 percent of all renters — were behind on their rent payments. Half of these households (51 percent) are families with children and we estimate there are 6.9 million children living in these households. This represents an enormous number of renters and their children who are now at risk of eviction and displacement, approaching the scale of the 2008 foreclosure crisis in which nearly 8 million households lost their homes.

Data on the share of households behind on rent comes directly from the Census Pulse survey, which has been asking the question “Is this household currently caught up on rent payments?” every two weeks since mid-August 2020.

The rent debt crisis has not abated over the past four months.

Fourteen percent of renter households were behind on rent the first time the Pulse survey posed this question. The share behind climbed up to 19 percent at the height of the pandemic and economic crisis in January, then crawled back down to 14 percent in March, where it has lingered for the past four months. This is likely about twice the pre-pandemic baseline: the 2017 American Housing Survey found that about seven percent of renters were unable to pay some or all of their rent.

Under the Trump administration, the federal government did not provide any direct resources for rental assistance for the first nine months of the crisis, but in December and January, Congress allocated $46.5 billion toward emergency rental assistance to be distributed by state, local, and tribal governments. By the end of July, however, only $5.1 billion of this rental assistance had been distributed. As our trend data show, these resources are not yet having a measurable impact on renters who are struggling to get out of debt.

There are six states where at least one in four low-income renters are behind on rent.

The share of renters who are behind on rent is much higher than the national average in some communities. At least one in four low-income renters are behind on rent in Georgia, Maryland, Pennsylvania, New Jersey, New York, South Carolina, and the District of Columbia. New York has the highest share of low-income renters with arrears (31 percent), followed by New Jersey (30 percent), and South Carolina (28 percent). Less than ten percent of low-income renters owe back rent in the states of Arizona, Idaho, Montana, Utah, and Wyoming.

In terms of sheer numbers, the most populous states are home to the most at-risk households: there are 2.6 million low-income renter households with debt living in California, New York, Texas, Florida, Pennsylvania, Georgia, and Illinois.

Among the 15 metros included in the Pulse survey, New York has the highest share of low-income renters with debt (32 percent), followed by Houston and Washington DC (28 percent). New York is home to the most low-income renters with debt by far (539,600 households), followed by Los Angeles (226,600 households).

Nationally, we estimate that rent debt amounts to $16.8 billion.

According to our estimates, total rent debt is $16.8 billion nationwide. On average, renters are behind three months’ rent and owe $2,730, but these averages mask much higher debts and levels of need for many renters, especially those with the lowest incomes. This is due to two factors. First, renters in higher-cost communities are paying higher rents thus will owe higher amounts: the average debt in the San Francisco Bay Area is $4,660. Second, the lowest income renters are more likely to be much further behind on rent and owe the most back rent. Based on the Pulse survey’s newly-added question about how many months renters with arrears are behind, 44 percent of renters are one month behind, 30 percent are two months behind, 12 percent are three months behind, 12 percent are between four and seven months behind, and 10.5% are eight to 16 months behind. Among low-income renters, one in four (25 percent) are at least four months behind, compared to 13 percent of renters with incomes above $50,000 per year. Low-income renters who are further behind owe greater debts: those who are eight or more months behind owe $9,435 on average (and in the Bay Area, its an average of $14,076).

The vast majority of those who are behind on rent are low-income households who lost jobs and income during the pandemic.

The overwhelming majority of households with debt — 84 percent — are low-income households with earnings of less than $50,000 per year, which is generally the group targeted by federal rental assistance programs. Nationwide, one in five low-income households are behind on rent.

Today’s rent debt crisis is entirely a consequence of the pandemic’s economic fallout: 68 percent of those who were behind on rent in May had lost employment income at some point during the pandemic, according to the May 12-24 Pulse survey. As our other research has shown, low-wage workers, who are disproportionately workers of color, were hardest hit by pandemic job losses and are most likely to suffer from rent debt. Currently, the majority of renters with arrears were not employed within the past week (55 percent).

Renters have made tremendous sacrifices and tradeoffs to stay current on rent, including foregoing medical care, delaying payment of other bills, eating cheaper (and potentially less healthy) food, and voluntarily moving in with friends and family — increasing their risk of Covid-19 exposure while losing their housing stability. The May 12-24 Pulse survey data showed that among low-income households who lost employment income at some time during the pandemic, 73 percent were current on rent. This underscores how paying rent has remained a top priority for all renters throughout the pandemic, despite the moratoria on evictions.

Renters of color have been disproportionately impacted by the pandemic and are more likely to owe back rent, making them more vulnerable to eviction risk.

Workers of color were hardest hit by the pandemic job losses and thus more likely to fall behind on rent through no fault of their own. Two-thirds of renters with arrears (66 percent) are people of color. Today, 26 percent of Black renters, 19 percent of Latinx renters, 19 percent of multiracial renters, and 17 percent of Asian or Pacific Islander renters are behind on rent, compared to 10 percent of White renters.

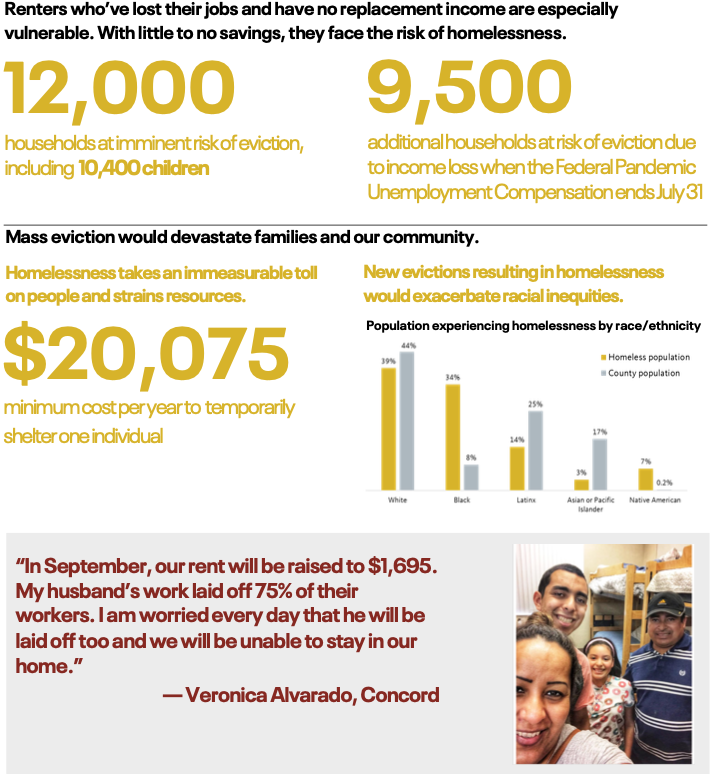

Among renters with arrears, Black renters disproportionately expect to be evicted by October: 56 percent of Black tenants with rent debt say they are very or somewhat likely to be evicted, compared with 45 percent of their White counterparts. Other research has shown that Black renters, especially Black women with children, are more frequently evicted by their landlords.

In the United States, renters have little housing security, paltry savings, and few legal protections from exorbitant rent increases or eviction (outside of a few states and cities with strong tenant movements). The rent debt crisis adds another layer to these preexisting inequities. Renters were already in crisis when the pandemic began: about a third of White renters and just under half of Black and Latinx renters were both economically insecure (earning less than 200 percent of the federal poverty level) and rent burdened (paying more than 30 percent of their income on rent). Gender is another important axis: women of color are most likely to be rent burdened, and disproportionately face eviction.

Rent debt is also contributing to the growth of the racial wealth gap. Historic and continuing housing and lending discrimination, as well as systemic inequities in the labor market, have contributed to large racial inequities in homeownership. (Atlas data show that seven in 10 White households own their homes while the majority of Black and Latinx households rent.) While renters, predominantly people of color, currently hold $17 billion in rent debt alone (not including utilities and other debts), homeowners, who are predominantly White, saw a $1.9 trillion increase in their home equity from the first quarter of 2020 to the first quarter of 2021 as competition for a constrained supply of homes drove prices up.

Rental assistance is not sufficiently reaching tenants in need.

Over the past month, the federal government has sought to speed up the distribution of rental assistance and the pace picked up in July, but only 11 percent of the allocated resources have been distributed as of the end of July. Our analysis of Treasury data tracking the distribution of the first round of assistance (ERA1) finds that there are 191 cities and counties where less than 25 percent of the funds have been distributed. This list includes many communities with large populations of low-income renters, such as Broward County, Florida; Chicago; Dallas (city and county); King County, Washington; and Los Angeles (city and county).

With the sluggish distribution of rental assistance, millions of renters are in limbo.

The rollout of emergency rental assistance has been riddled with challenges including complicated and confusing application processes, which the Treasury is now seeking to streamline, as well as the refusal of some landlords to participate. In August, the Pulse survey added a question about the status of rental assistance for households with arrears. This new dataset provides insight into how these programs are working and illustrates many of the challenges that renters face in accessing these resources. Nationwide, one in five renters with debt (22 percent) have applied for rental assistance and are awaiting a response. Three in five (62 percent) have not yet applied for rental assistance. One in ten (12 percent) applied for and were denied rental assistance.

Rent is not the only debt accumulating for renters.

While our analysis focuses on back rent, renters’ pandemic debt crisis extends far beyond their obligations to their landlords. Many renters are borrowing from family and friends or taking on other forms of debt in order to make rent and pay for household expenses. A University of Pennsylvania survey of California renters who applied for rental assistance found that the majority had about $3,050 in “shadow debt” they borrowed to pay their rent that is not covered by relief programs.

According to the Pulse survey, among households behind on rent, 51 percent borrowed from friends or family to pay rent, compared with 14 percent of households current on rent. About 30 percent of all renter households used a credit card (or some other form of debt) to pay rent. Many are behind on other bills, such as utilities or car payments. A survey of water debt in California found that 1.6 million households owed $1 billion on water bills — $500 on average; and in Massachusetts half a million households were 90 days behind on their utilities, averaging $1,000 in debt.

Eliminating Rent Debt is an Equity Imperative and a Moral, Economic, and Public Health Necessity

Today’s rent debt crisis is a microcosm of the wretched inequality of the pandemic: millions of renter households — most of them people of color — now face the burden of owing back rent and the risk of being evicted due to a public health crisis that upended their finances. These unequal consequences are not random, but the predictable result of past policies that left millions of families with no savings to draw upon in the face of an economic shock, as well as the failed early policy response to the pandemic. Although the CARES Act provided important unemployment benefits and cash assistance as well as an eviction moratorium that helped many pandemic-impacted renters, undocumented and mixed-status families were ineligible for assistance and the moratorium ended in July of 2020, leaving renters unprotected until the CDC enacted its moratorium in early September of last year. Moreover, absent meaningful financial assistance to pay back-rent, the moratorium simply delayed eviction, yet the federal government provided no rent relief until December.

Swiftly clearing rent debts is urgently needed to stave off mass eviction, which would directly harm economically vulnerable families and their communities and have long-term ripple effects throughout communities and our economy. Eviction has significant and undeniable negative consequences for mental and physical health, educational outcomes, and household finances. Amidst the continued spread of the Delta variant, evictions will have disastrous impacts on public health: Research during the pandemic found that states that allowed evictions to proceed had more Covid infections and deaths than those with eviction moratoria. And particularly at a time when rents are increasing everywhere, eviction will increase homelessness, with its devastating consequences for health and well-being and significant costs for local governments.

Forgiving rent debt is also essential to an equitable and people-centered recovery: one in which those hardest-hit by the pandemic can fully participate and thrive.

Policymakers Must Take Immediate Action to Prevent Eviction and Clear Rent Debt

The new data underscores the magnitude of the rent debt crisis in communities across the country and the urgency of providing eviction protections and distributing rental assistance to avert the specter of mass eviction and skyrocketing homelessness. Targeted support is particularly needed in places with the most low-income renters with debt, slowest distribution of rental assistance, and weakest tenant protections. But no community is immune to the rent debt crisis. Policymakers everywhere should partner with community-based organizations that have been working with the communities most impacted by both the pandemic and systemic racism to address this immediate crisis and implement long-term solutions to housing insecurity.

At the federal level, Congress should act immediately to pass a national eviction moratorium that lasts through the end of the pandemic. This will give states and local governments the necessary time to deliver rental assistance to those in need. HUD and FHFA should enact an eviction moratorium for all renters living in all federally assisted properties and urge the administration to explore and use any authority it has to institute a moratorium or other eviction prevention requirements on properties that have a federally backed mortgage or multifamily loan. The Department of Justice and Treasury should use their authority to ensure that renters eligible for relief get assistance quickly and are not moved through the court eviction process.

State and local governments and their courts must double down on the important work they are doing by partnering with directly impacted communities and renter advocates to pass and strengthen eviction and utilities shutoff moratoria, streamline the delivery of rent relief, provide access to free legal assistance for renters facing eviction, establish eviction diversion programs. In the absence of moratoria, they should require landlords to apply for rental assistance as a condition of filing evictions (for any reason, not only nonpayment of rent), ensure that renters who’ve applied for assistance are protected from eviction, and extend rent repayment periods for renters who do not receive assistance.

Localities should disaggregate their data on rent relief program performance by geography, income, and race/ethnicity, and make it accessible to housing assistance providers and the general public. Presenting this data in dashboards is critical but insufficient: the data should be provided in downloadable spreadsheets or databases that can be analyzed to inform outreach and assistance efforts and hold leaders accountable for delivering assistance. Localities should also track and democratize data on evictions and rental ownership patterns with a focus on which landlords are responsible for evictions in order to develop long-term policy solutions to prevent eviction and stabilize renters, particularly as recent data indicate an increase in institutional investor ownership through the pandemic and link between corporate landlords and higher rates of eviction.

For more local policy ideas and examples, see https://ourhomesourhealth.org.